Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. aspernatur aut odit aut any anyaspernatur aut odit autaspernatur aut odit autaspernatur aut odit

Nemo enim ipsam voluptatem quia voluptas sit aspernatur aut odit aut fugit, sed quia consequuntur magni dolores eos qui ratione voluptatem sequi nesciunt. Neque porro quisquam est, qui dolorem ipsum quia dolor sit amet, consectetur, adipisci velit, sed quia non numquam eius modi tempora incidunt ut labore et dolore magnam aliquam quaerat

"class="material with-radius">The introduction of Corporate Tax (CT) in the UAE marked a pivotal advancement in the nation’s tax framework. With the assumption that registration processes are complete, the focus now shifts to the critical aspects of CT return filing, including adherence to submission deadlines, compliance with regulatory criteria, and fulfillment of documentation requirements. Accurate and timely filing remains essential to ensuring compliance and mitigating potential liabilities.

">

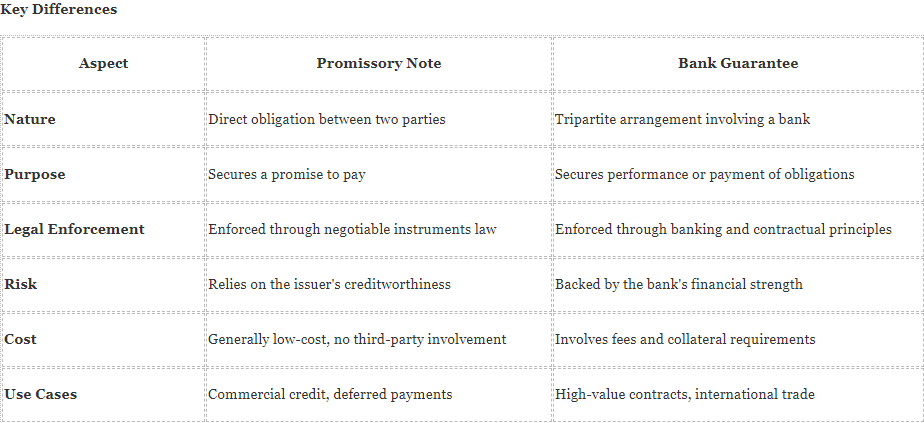

Both promissory notes and bank guarantees are powerful financial instruments when properly utilized. However, their effectiveness depends on meticulous drafting, compliance with Saudi legal requirements, and the specific circumstances of the transaction. Legal consultation is essential to ensure that these instruments are tailored to the needs of the parties and provide the intended level of protection.

As a legal consultant with expertise in Saudi financial law, we emphasize the importance of understanding not only the technical distinctions between these instruments but also their practical implications in the Kingdom’s dynamic legal and commercial environment. For businesses operating in Saudi Arabia, selecting the appropriate instrument can mitigate risks and facilitate successful transactions in both domestic and international markets.

Thomas Paoletti

Francesca Romana Valeri

"class="material with-radius">

Both promissory notes and bank guarantees are powerful financial instruments when properly utilized. However, their effectiveness depends on meticulous drafting, compliance with Saudi legal requirements, and the specific circumstances of the transaction. Legal consultation is essential to ensure that these instruments are tailored to the needs of the parties and provide the intended level of protection.

As a legal consultant with expertise in Saudi financial law, we emphasize the importance of understanding not only the technical distinctions between these instruments but also their practical implications in the Kingdom’s dynamic legal and commercial environment. For businesses operating in Saudi Arabia, selecting the appropriate instrument can mitigate risks and facilitate successful transactions in both domestic and international markets.

Thomas Paoletti

Francesca Romana Valeri

">

"class="material with-radius">

">

"class="material with-radius">

">

"class="material with-radius">

">

"class="material with-radius">

">"class="material with-radius">">

Thomas Paoletti

Francesca Romana Valeri

"class="material with-radius">

Thomas Paoletti

Francesca Romana Valeri

">Thomas’ participation highlighted our ongoing commitment to staying at the forefront of legal and business practices, ensuring we continue delivering the best service to our clients worldwide. We are excited about the innovative ideas and opportunities gained from this global gathering, and we look forward to reconnecting with our network friends, and connections at the next IR Global conference.

Thomas Paoletti

Paoletti Law Group

"class="material with-radius">Thomas’ participation highlighted our ongoing commitment to staying at the forefront of legal and business practices, ensuring we continue delivering the best service to our clients worldwide. We are excited about the innovative ideas and opportunities gained from this global gathering, and we look forward to reconnecting with our network friends, and connections at the next IR Global conference.

The dispute is on employment matters, and the parties elected the SCT as dispute resolution forum,

The amount of claim is less than AED 1,000,000 and the parties to the dispute have themselves submitted its jurisdiction.

Tribunal Fee

In employment matters the SCT charges a fee of 2% of the value of the claim with a minimum of USD 100. Any appeal of a decision made by the SCT in the Court of First Instance (CFI) may be subject to a fee of 1% of the dispute at the CFI.

For rental disputes that do not exceed AED 500,000, the SCT may charge a fee of 5% of the disputed amount with a minimum of USD 100. For other disputes, the SCT may charge a fee of 5% as a Tribunal fee for adjudicating the claims. For such disputes, the appeal to the CFI shall be subject to a fee of 2.5% of the disputed amount.

Procedural Brief

Below are a few features of interest in how the SCT functions:

The parties need not be represented by lawyers and must represent themselves. Alternatively, a non-lawyer representative may appear before the SCT with a power of attorney. A company may be represented by an authorized representative to appear before the SCT. There is an express need to take permission from the SCT Judge to be represented by a lawyer.

The SCT has a set timeline of seven days in which the defendant upon service of the claim has to respond to the claimant and file his defense with the SCT.

After the filing of claims and counterclaims, the SCT Registry appoints a pre-hearing consultation in which the SCT Judge tries to resolve the dispute before initiating the trial.

In the absence of any of the parties during the consultation process, the SCT Judge may pass an adverse order against the parties wherein the claim may be settled in favor of the claimant (in the defendant’s absence) or the claim may also be dismissed (in the claimant’s absence). The Judge may also choose to adjourn the matter to another date. Hence it becomes important for the parties to explain their absence in advance to avoid adverse order.

If the parties fail to settle the matter during consultation, the SCT Judge may direct the parties to prepare the claim for hearing.

A different SCT judge is appointed to preside over the hearing and he chooses the method and procedure for the proceedings.

The Parties have to attend the hearings and present their cases personally. The SCT judge may allow the parties to be represented by non-lawyers where reasonably necessary. Legal representation is only allowed in exceptional cases.

Any party may file an appeal against the decision of the SCT and has to seek Permission to Appeal which has to be approved by CIF before the appeal proceedings are initiated in the CIF.

Thus, the DIFC SCT has greatly contributed towards making the resolution of disputes a very simple and fast process.

The dispute is on employment matters, and the parties elected the SCT as dispute resolution forum,

The amount of claim is less than AED 1,000,000 and the parties to the dispute have themselves submitted its jurisdiction.

Tribunal Fee

In employment matters the SCT charges a fee of 2% of the value of the claim with a minimum of USD 100. Any appeal of a decision made by the SCT in the Court of First Instance (CFI) may be subject to a fee of 1% of the dispute at the CFI.

For rental disputes that do not exceed AED 500,000, the SCT may charge a fee of 5% of the disputed amount with a minimum of USD 100. For other disputes, the SCT may charge a fee of 5% as a Tribunal fee for adjudicating the claims. For such disputes, the appeal to the CFI shall be subject to a fee of 2.5% of the disputed amount.

Procedural Brief

Below are a few features of interest in how the SCT functions:

The parties need not be represented by lawyers and must represent themselves. Alternatively, a non-lawyer representative may appear before the SCT with a power of attorney. A company may be represented by an authorized representative to appear before the SCT. There is an express need to take permission from the SCT Judge to be represented by a lawyer.

The SCT has a set timeline of seven days in which the defendant upon service of the claim has to respond to the claimant and file his defense with the SCT.

After the filing of claims and counterclaims, the SCT Registry appoints a pre-hearing consultation in which the SCT Judge tries to resolve the dispute before initiating the trial.

In the absence of any of the parties during the consultation process, the SCT Judge may pass an adverse order against the parties wherein the claim may be settled in favor of the claimant (in the defendant’s absence) or the claim may also be dismissed (in the claimant’s absence). The Judge may also choose to adjourn the matter to another date. Hence it becomes important for the parties to explain their absence in advance to avoid adverse order.

If the parties fail to settle the matter during consultation, the SCT Judge may direct the parties to prepare the claim for hearing.

A different SCT judge is appointed to preside over the hearing and he chooses the method and procedure for the proceedings.

The Parties have to attend the hearings and present their cases personally. The SCT judge may allow the parties to be represented by non-lawyers where reasonably necessary. Legal representation is only allowed in exceptional cases.

Any party may file an appeal against the decision of the SCT and has to seek Permission to Appeal which has to be approved by CIF before the appeal proceedings are initiated in the CIF.

Thus, the DIFC SCT has greatly contributed towards making the resolution of disputes a very simple and fast process.

"class="material with-radius">The IPO boom in the UAE is poised to reshape the country’s economic landscape and propel it as a global investment destination.

The positioning of the United Arab Emirates (UAE) as a global economic powerhouse by the government through economic diversification and government investment has ensured that the country experiences strong economic growth despite global slowdowns. With a prime focus on economic diversification, the country has seen increased investment in sectors such as tourism, real estate, logistics, financial services and technology-related markets.

Several attractive tax initiatives have drawn young entrepreneurs across the world to make the country their base for business operations, turning the UAE into a regional and global leader in investments in private and public companies. Given the dynamics of the economic landscape, the UAE has emerged as a prominent destination for initial public offerings (IPOs), which reflects the country’s commitment to fostering a robust capital market and attracting global investment.

It is pertinent to analyze the yearly surge in the value of IPOs in the UAE. In 2008, the UAE saw in total six IPOs of a total value of close to a billion dollars. In 2022, the UAE from its 11 issuances saw proceeds of around $ 13.96 billion.

In 2023, UAE firms raised $ 6.07 billion from the eight IPOs that were listed. Although this was a decline from the previous year, the UAE was the most dominant among the GCC countries as this accounted for 56.3 percent of the region’s total issuance proceeds.

In 2024, the Abu Dhabi Stock Exchange may expect listings of private companies including Lulu Group, Spinneys Dubai, Dubai Parkin and Advanced Inhalation Rituals.

Factors behind the surge

The notable increase in the IPOs in the UAE can be attributed to various factors, including the government’s focus on diversification, political stability, financial regulatory reforms and the UAE’s strategic location and position as a global and financial business hub. The IPOs in the UAE have attracted substantial interest from both the retail and institutional investors, resulting in multifold over-subscription and reflecting the region’s growing investor appetite for the emerging growth opportunities.

The UAE’s adoption of international standards in respect of regulatory and market frameworks has helped it to witness massive investments from across the world. Further initiating favourable tax and economic policies has helped the country create a stable business landscape for entrepreneurs and established businesses. Initiatives like Dubai free zones and favourable taxation for foreign investors have led to the UAE accounting for over 30 percent of the foreign direct investment inflow to the MENA region.

The IPO eligibility rules in the UAE only allow profitable entities to be listed on the stock exchange. For onshore companies, the Security and Commodities Authority (SCA) requires the business to show a net operational profit of at least ten percent of the company’s capital for the past two years.

For other companies established in the offshore economic free zone, the criteria are to show profitability for the last two years to get listed on the stock exchanges of Dubai International Financial Centre (DIFC) and Abu Dhabi Global Market (ADGM). Unlike the mainland, there are no minimum criteria for profit to get listed. Most of the recent IPO candidates in the UAE have come from these free zones.

It is argued by some that the removal of the profitability requirement may boost the number of IPOs as several tech corporations in their initial phases are more focused on growth than on profitability. Companies such as Google, valued stocks today, were unprofitable for years. The criteria of minimum profitability for IPOs denies such technology companies investment opportunities through IPOs.

Transparency with growth

The UAE law also enforces several stringent post-IPO regulations. These involve accelerated financial reporting timelines wherein listed companies must disclose their quarterly earnings within 45 days following the end of the reporting period and must report audited financial statements within 90 days from the end of the financial year. Any delay in meeting deadlines may result in a damaging reputation and suspension of the share trading license.

Further, the listed companies must rotate their auditors in line with the SCA rotation rules wherein audit engagement partners have to be changed every three years and the audit firm is to be rotated every six years.

These rules are being enforced to bolster transparency and accountability, as well as to promote independence and objectivity in the UAE’s finance market. With the country positioned as a hub of innovation, the continuous expansion of the IPO market requires the UAE to fortify its reputation globally, wherein the finance teams of these companies are being asked to be more strategic, digital and investor-friendly.

The surge in IPOs in the UAE mirrors the country’s evolution into a dynamic financial hub driven by a range of factors, including economic diversification efforts, regulatory reforms and technological advances. As companies seize the opportunity to access public markets and investors capitalize on the region’s growth potential, the IPO boom in the UAE is poised to reshape the country’s economic landscape and propel it as a global investment destination.

"class="material with-radius">The United Arab Emirates (UAE) stands as a beacon of economic promise in the Gulf, magnetizing global entrepreneurs and businesses with its strategic location, vibrant marketplace, and favorable business environment.

For UK enterprises eyeing expansion into the Middle East, the UAE offers a wealth of opportunities that have flourished in recent years. However, conquering this bustling market demands meticulous planning, cultural savvy, and strategic execution.

Here are 10 indispensable guidelines to navigate the journey of establishing your presence in the UAE:

Dive into Comprehensive Market Research

Understanding the intricacies of the UAE market is paramount before embarking on your business venture. Delve into market dynamics, consumer behaviors, and competitive landscapes to identify viable opportunities and potential challenges. Familiarize yourself with local regulations, business norms, and cultural nuances that shape business operations.

Choose the Right Business Structure

Selecting the appropriate business framework is crucial for success in the UAE. Options range from establishing a mainland company to opting for a free zone setup with tax benefits and full foreign ownership. Evaluate your choices carefully to align with your business goals and navigate regulatory requirements effectively.

Seek Expert Guidance

Navigating the legal and bureaucratic landscape of the UAE can be complex. Engage legal professional with expertise in the region to guide you through company formation, licensing, visa processes, and compliance matters.

Build Strong Local Partnerships

Cultivating alliances and partnerships is key in the UAE. Consider collaborating with local sponsors, distributors, or agents who possess market insights, networks, and cultural sensitivity. Partnering with esteemed local entities can accelerate market entry, enhance credibility, and unlock new opportunities.

Embrace Cultural Sensitivity

Respect for local customs, traditions, and business etiquette is essential for building trust and fostering successful business relationships in the UAE. Invest in cross-cultural training for your team to bridge communication gaps and promote mutual understanding.

Prioritize Compliance and Transparency

Adhering to UAE laws and regulations is fundamental for conducting business operations smoothly. Stay updated on legal requirements related to company registration, licensing, taxation, employment, and intellectual property rights. Uphold transparency and ethical business practices to earn trust and credibility.

Harness Digital Advancements

Embrace digitalization to drive operational efficiency and innovation. Leverage technology to streamline processes, enhance customer engagement, and optimize marketing strategies. Invest in robust cybersecurity measures to safeguard data and mitigate cyber risks.

Flexibility

Adaptability is key in the UAE’s dynamic business environment. Be prepared to adjust strategies in response to market shifts, emerging trends, and geopolitical developments. Maintain agility and resilience to navigate uncertainties and seize new opportunities.

Deliver Exceptional Customer Service

Customer satisfaction is paramount in the UAE, where discerning consumers expect top-notch products and services. Prioritize personalized solutions, responsive support, and seamless transactions to enhance customer experience. Utilize customer relationship management tools to foster engagement and loyalty.

Foster a Culture of Innovation

Cultivate a culture of creativity, innovation, and continuous improvement within your organization. Encourage experimentation and risk-taking to stay ahead of the competition. Empower employees to contribute to company growth and success through innovation.

In conclusion, venturing into the UAE market offers UK businesses a gateway to expansion and growth in the Middle East. By following these guidelines and leveraging expert advice, cultural awareness, and adaptability, entrepreneurs can navigate the nuances of the UAE business landscape and establish a strong presence in this dynamic market. With perseverance, strategic foresight, and a commitment to excellence, UK enterprises can thrive and excel in the UAE’s diverse and vibrant economy.

How are global geopolitical events affecting mobility in your jurisdiction?

Geopolitical instability generally influences mobility. However, emigration does not come exclusively from conflict zones, and can be purely economic.

The immigration policies of the UAE intend to attract skilled professionals. The policy has helped the UAE attract exceptional talent.

The UAE has a safety index of 84.9 and is considered one of the safest countries in the world. Three of its cities are in the top five safest globally. The major attraction that immigrants find in the country is its openness and commitment to pluralism, and it is home to a 90% foreign population,

Q2

Climate concerns are increasingly becoming a decision-making factor in global migration – how is this impacting your jurisdiction?

The entire GCC region is likely to face a climate crisis as many climate-related studies have pointed to the fact that there shall be an increase in temperature up to 5 degrees in the GCC region by the end of this century, meaning that local populations, including in the GCC, will face major health and livelihood challenges in the coming future. As many as 400 million inhabitants of the Middle East will be at risk of exposure to extreme heat waves that may also stoke social and political tensions.

The UAE’s government has been very keen to address global concerns over climate change and has acted to reduce its carbon footprint and the dependence of its economy on fossil fuels. The same is evident from the UAE hosting the recently held COP28 (United Nations Climate Change Conference or Conference of the Parties of the UNFCCC).

The UAE has been at the forefront of acting on climate policies and has set the target of 2050 for the goal of net zero emissions. However, resource-rich countries like the UAE will experience an increase in the rate of immigration from poorer regions despite their own forecasted climatic challenges. The GCC could potentially receive some of the 143 million climate migrants from Southeast Asia, Sub-Saharan Africa, and Latin America, that the World Bank expects could be displaced by 2050.

Q3

How is government policy influencing mobility in your jurisdiction – particularly regarding employment relocation?

The UAE government has introduced massive changes to its labour laws through Federal Decree Law No 33 of 2021. The new law aims to enhance the nation’s labour market’s elasticity, resilience, and sustainability and promote a flexible and competitive business environment for the next 50 years.

Additionally, with these new laws and visa regulations, the UAE is working to create a welcoming environment for foreign individuals and investors, further solidifying the UAE’s position as an attractive destination for living and conducting business.

The law prohibits discrimination, forced labour, harassment and bullying; some of the other new developments in the labour laws that shall apply to private sector employees is the introduction of temporary and flexible work models to allow flexible hiring and working practices.

Furthermore, recent legislative changes have seen an increase in maternity leave provisions, reflecting the government’s commitment to supporting family life and gender equality. Additionally, other initiatives, such as enhanced quality-of-life measures, have been introduced to create a holistic and inclusive environment, making the UAE an even more desirable destination for individuals seeking not only professional opportunities but also a higher quality of life.

Further, the UAE government has made it easier for freelancers to migrate to the jurisdiction by introducing Freelancer Visa. This Visa allows self-employed individuals to sponsor themselves. Workers in the UAE and overseas in specialised fields such as blockchain, AI, and digital currencies can access the freelancer visa.

The new labour law also lays certain obligations on employers, which include providing accommodation, training and other means to ensure the safety and welfare of the employees through insurance, healthcare costs and other entitlements to the employee’s.

Thomas will open the conference with his ‘Welcome to Dubai’ presentation on the investment opportunities in Dubai, focusing on key topics such as ESG, Artificial Intelligence and strategic sectors, with Francesca leading a breakout session exploring ‘Global Talent Strategy.’

For those attending, we look forward to welcoming you to Dubai!

"class="material with-radius">Thomas Paoletti and Head of Legal for the Middle East Francesca Romana Valeri, will be hosting talks during the event.

Thomas will open the conference with his ‘Welcome to Dubai’ presentation on the investment opportunities in Dubai, focusing on key topics such as ESG, Artificial Intelligence and strategic sectors, with Francesca leading a breakout session exploring ‘Global Talent Strategy.’

"class="material with-radius">The United Arab Emirates (UAE) is set to host the 28th Conference of the Parties (COP 28). This crucial gathering brings together nations worldwide to address the pressing climate change issues.

This isn’t just any meeting; it’s a chance to make some real progress in the fight against climate issues. Think of it as a turning point. The action unfolds in Dubai from November 30th to December 12th, 2023.

Get ready for something special – it’s not just a conference; it’s a step toward a greener future for everyone and we will keep you posted!

Leadership for COP 28

Dr. Sultan Ahmed Al Jaber is leading the conference as the President-Designate for COP28 UAE. As the Abu Dhabi National Oil Company (ADNOC) CEO, he led a $15 billion decarbonisation strategy and has been an industry pioneer in leading renewable energy initiatives.

Youth Climate Champion has been designated to the Minister of Community Development of UAE, H.E. Shamma Al Mazrui. As Youth Climate Champion, she will engage with local and global stakeholders to provide opportunities for the young in renewable energy roles.

Further, H.E. Razan Al Mubarak will be acting as the UN Climate Change High-Level Champion, and she will be mobilising with different state and non-state actors to promote a unified approach to reach global goals on climate change.

H.E. Mariam Almheiri, as the UAE Minister of Climate Change and Environment, shall support the team of COP 28 and shall ensure that the UAE delivers on its climate targets set out by the Paris Agreement and its Net Zero 2050 strategy.

The Choice of the UAE

The selection of the UAE as the host country for COP 28 is significant for several reasons. Despite being an oil-rich nation, the UAE has proactively diversified its economy and invested in renewable energy. Hosting COP 28 allows the UAE to showcase its commitment to sustainable development and its efforts to transition towards a green economy.

The country’s strategic location also plays a role. The Middle East is particularly vulnerable to the impacts of climate change, from rising temperatures to water scarcity. By hosting COP 28, the UAE emphasises the importance of addressing climate change as a global challenge that requires collective action.

Platforms for Dialogue-Blue Zone and Green Zone

With the expected participation of over 70,000 participants, including heads of state, government officials, industry leaders, academics, and representatives from non-accredited delegates and other voice organisations,

Blue Zone is a UNFCC-managed site open only to nation-state delegates, Observers (NGOs, IGOs, UN Agencies), Media and other World Leaders.

Green Zone, on the other hand, is a space managed by the COP28 UAE Presidency, and it aims to offer a platform to non-accredited delegates like youth groups, civil society, NGOs, the private sector and indigenous groups to have their voices heard and to promote dialogue.

Key Themes and Agendas

COP 28 is expected to focus on a range of critical themes, building on the outcomes of previous conferences. One of the central discussions will revolve around efforts to limit global warming to well below 2 degrees Celsius above pre-industrial levels, as outlined in the Paris Agreement. Countries will be urged to enhance their climate action plans, known as Nationally Determined Contributions (NDCs), to align with this goal.

Renewable energy and decarbonisation will also be in the spotlight. The UAE, known for its ambitious clean energy initiatives, will likely showcase its progress. The conference will explore ways to accelerate the transition to renewable energy sources and reduce reliance on fossil fuels.

Will the World leaders commit more this time?

There has been constant criticism of the leaders attending the COP every year for their refusal to commit more to the cause of achieving the goals of the Paris Agreement, which aimed at reducing the increase in temperature to 2°C or 1.5°C by the end of the century. Civil society around the world shall keep an eye on leaders across the world visiting the COP 28 with an expectation of ambitious goals for countries to achieve individually.

Global Decarbonization Alliance

Another highlight of the event is the involvement of industrialists in the meeting. Indeed, the President of COP 28, as previously noted, also serves as the CEO of ADNOC. This holistic strategy, bringing together leaders from the oil and gas sector and high-emitting industries, alongside global decision-makers, holds promise for long-term success. The President’s primary initiative involves encouraging oil and gas companies to commit to robust climate pledges and unite in establishing a Global Decarbonization Alliance.

Conclusion

COP 28 in the UAE holds great promise for advancing global efforts to combat climate change. As nations come together to negotiate and collaborate, the conference provides an opportunity to reinforce the shared commitment to creating a sustainable and resilient future. The outcomes of COP 28 will not only shape the international climate agenda. Still, they will also determine the trajectory of our planet’s response to one of the greatest challenges of our time.

To read the full IR Global Publication, kindly click here

"class="material with-radius">Current Appetite for Investment in Foreign Companies in UAE

In recent years, the United Arab Emirates (UAE) has witnessed a growing appetite for investment in foreign companies, particularly in its economic heart, Dubai and Abu Dhabi. The nation’s strategic location, robust infrastructure, investor-friendly policies, and stable business environment have positioned it as an attractive destination for global investors seeking lucrative opportunities. The emirate of Dubai’s thriving economy, diverse sectors, and commitment to innovation have further bolstered its allure for foreign investments. Foreign direct investment (FDI) inflows into the UAE have remained consistently high, reflecting investor confidence in the nation’s economic prospects. A proactive and progressive government approach, coupled with a strong regulatory framework, has provided investors with a sense of security

and stability. Additionally, the UAE’s robust trade relations with various countries have facilitated increased investment flows into the Emirates.

Impact of Global Geopolitical and Economic Fluctuations on Commercial Engagements in UAE

Despite UAE’s resilience, the global geopolitical and economic fluctuations have not left the emirate untouched. These fluctuations, ranging from trade tensions to technological disruptions and pandemics, have led to uncertainties and challenges for businesses operating in the UAE. However, the UAE’s dynamic and diversified economy, in the different emirates, has played a crucial role in mitigating some of the adverse effects. Global geopolitical tensions have at times resulted in trade disruptions and fluctuations in commodity prices, which

can impact businesses operating in the UAE. Additionally, the fluctuating economic landscape can influence investor sentiments, causing some degree of cautiousness in investment decisions. However, the UAE’s strategic initiative and commitment to diversification have enabled it to proactively respond to such fluctuations and emerge resiliently.

Attracting Interest and Securing Funding from Investors in the UAE

Businesses seeking to attract interest and secure funding from investors in the UAE must adopt a strategic and proactive approach.

Below I summarize some key considerations to enhance investor appeal based on my experience in UAE:

• Market Research and Targeting: Comprehensive market research is essential to identify sectors and industries with strong growth potential. By honing in on specific market niches, businesses can tailor their commercial proposals to align with investor interests.

• Value Proposition and Differentiation: Articulating a clear and compelling value proposition is critical. Businesses must highlight their unique strengths, differentiators, and competitive advantages to stand out from the competition.

• Strong Financial Projections: Investors seek a thorough understanding of a company’s financial health and projections. Robust financial planning, based on accurate data and realistic assumptions, is crucial to instill invest or confidence.

• Transparency and Governance: Transparent and robust corporate governance practices are highly valued by investors. Companies must demonstrate a commitment to accountability, ethical practices, and risk management.

• Building Relationships: Cultivating strong relationships with potential investors is pivotal. Engaging in networking events, industry conferences, and business forums can foster connections and showcase the potential for fruitful collaborations.

In conclusion, based on my experience as a professional living in the UAE and with extensive experience in the UAE market and business, I bear witness to the remarkable transformation of the UAE into a global business powerhouse.

The current appetite for foreign investment in the emirate is a testament to its enduring allure as a strategic and investor-friendly destination.

While global geopolitical and economic fluctuations pose challenges, the UAE’s adaptability, visionary leadership, and steadfast commitment to diversification fortify its resilience in weathering uncertainties.

To attract interest and secure funding from investors in the UAE, businesses must approach their proposals with meticulous attention to detail. Thorough market research, a compelling value proposition, sound financial projections, robust governance, and proactive relationship building are essential elements that form the bedrock of a strong commercial proposal.

As the Emirates propels forward, businesses embracing a comprehensive and strategic approach, bolstered by legal clarity and compliance, will be at the forefront of UAE’s success story. As a legal consultant, I take pride in assisting companies in navigating the UAE’s business landscape, ensuring they can harness the limitless opportunities that the UAE presents.

TOP TIPS Building a strong commercial proposal for investors

Thorough Research: Conduct comprehensive research on the target market, competitors, and investor preferences to tailor the proposal accordingly.

Compelling Value Proposition: Clearly outline the unique selling points and the value the business brings to investors, emphasizing growth prospects.

Financial Prudence: Present well-structured financial projections, backed by accurate data, realistic assumptions, and a clear growth trajectory.

Governance and Ethics: Demonstrate a strong commitment to transparency, good governance, and ethical practices.

Engagement and Follow-Up: Actively engage with potential investors, respond promptly to inquiries, and follow up diligently to maintain interest.

“The nation’s strategic location, robust infrastructure, investor-friendly policies, and stable business environment have positioned it as an attractive destination for global investors.”

"class="material with-radius">Understanding EPC Contracts: A 360-Degree Perspective. What are we talking about?

EPC contracts epitomize a holistic project delivery approach, merging design, procurement, and construction under one umbrella.

EPC contracts represent a project delivery approach where a singular contractor is responsible for design, procurement, and construction. These contracts are mainly employed for intricate, large-scale endeavors, offering clients a centralized point of contact throughout the project lifecycle.

The International Federation of Consulting Engineers (FIDIC) has formulated a suite of standard contract forms for EPC projects, comprising the Red Book, Yellow Book, and Silver Book. The Red Book corresponds to conventional design-bid-build projects, the Yellow Book pertains to plant and design-build ventures, and the Silver Book caters to EPC turnkey undertakings.

Thorough scrutiny of the multifaceted EPC contract by both the client and contractor before signing is imperative. The document should precisely delineate the scope of work, the obligations of each party, payment terms, and procedures for dispute resolution.

EPC contracts present several merits, including consolidating responsibility under one entity and simplifying communication and coordination. Additionally, the efficiency of project completion is often heightened due to the integrated nature of the EPC contractor’s role. Moreover, a significant portion of risk can be shifted to the EPC contractor, safeguarding the client’s financial interests.

However, this contract type is accompanied by certain drawbacks, such as escalated costs due to the EPC contractor’s premium for undertaking increased risk. It also curtails flexibility for the client to effect changes post-contract signing, and the intricate nature of the EPC contract can potentially lead to interpretational conflicts between the parties.

EPC contracts present a versatile project delivery method suitable for diverse clients. Nevertheless, a meticulous assessment of its pros and cons is essential before adoption. Here are some key considerations:

Prioritize EPC contractors with a proven track record in similar projects.

Thoroughly review the contract to align with the needs of both client and contractor.

Clients must possess a comprehensive grasp of the risks associated with EPC contracts.

By adhering to these guidelines, clients can enhance the likelihood of successful EPC projects. The multifaceted nature of EPC contracts necessitates meticulous evaluation to ensure that project goals are achieved with minimized conflicts and optimized efficiency.

In the world of EPC, success demands a blend of strategy, experience, and legal finesse. At Paoletti Law Group, we stand by your side as stalwart navigators, propelling you toward triumphant project delivery. With FIDIC’s wisdom as our North Star and our team’s EPC triumphs as our compass, your journey is destined for excellence!

Stay tuned for the next edition, where we unravel more EPC mysteries and empower you with insights that matter.

"class="material with-radius">Right of retention on abandoned boats, self-protection for nautical companies

In Olbia training event organized by Confindustria Centro Nord Sardegna, together with Cna Gallura and Confartigianato Gallura; in collaboration with Paoletti Law Group

Olbia 24 July 2023. The phenomenon of boats left in a state of neglect (in shipyards or ports) is also widespread among the nautical companies of Gallura. A problem that companies are called to manage independently and that can also lead to holes in the balance sheet. However, there are tools that allow you to overcome the stalemate phase. The most effective and used is the “right of retention”, which consists of an action of self-protection to be initiated before the judicial bodies. On the subject, Confindustria Centro Nord Sardegna, together with Cna Gallura and Confartigianato Gallura; in collaboration with the associated firm Paoletti Law Group of Verona (which has a long experience in the field of maritime law), has recently promoted a training event aimed at operators in the sector.

In the conference room of the DoubleTree hotel in Olbia, lawyers Alberto Bardini and Sabrina Pangrazio took stock of the “right of retention”, illustrating the main solutions to be adopted to unblock situations of abandonment of boats in shipyards or ports, with a property completely disappeared or manifestly insolvent. These are in fact registered movable property, which often occupy precious space for other uses and which often constitute complicated cases to be solved, especially if the boat is from a non-EU country. In the face of liabilities for certain corporate realities caused precisely by situations of this type, there is also the further problem of the liability of the director of the company for lack of credit protection.

The only way to go is to see the ownership of the abandoned property recognized with the assignment of the boat to the shipyard, in order to return from the expenses. In short, it is a matter of obtaining an asset that can then be sold or used to cover the loss occurred over the years for custody in the shipyard or in the port.

Flags of convenience

Complicating the picture, however, is the problem of the “flags of convenience” of certain boats. If the flag is of an EU state, the procedure is clear. If it is other states; the example of a boat flying the British flag but from the crown islands, such as Man or Jersey; A highly qualified legal specialization is required to unravel the issue and allow the judge to apply foreign law, as required by the rules, and resolve the judgment.

The procedures of release or assignment of ownership to the shipyard of abandoned boats are also applied in the Sardinian courts; in particular in that of Tempio Pausania, competent for the north-east of the island, as was recalled during the meeting. It ended with the interventions of the operators of the sector who formulated several questions confirming the topicality of the problem analyzed.

"class="material with-radius">The United Arab Emirates, with its investor-friendly policies, is the world’s third fastest emerging economy according to the Foreign Direct Investment Confidence Index.

While the United Arab Emirates (UAE) has rapidly emerged as one of the most attractive business economies for investors in recent years, thanks to the country’s strategic location, stable economy and favourable business policies, at the same time it is moving towards stricter compliance rules to curb illegal activities.

Has the UAE got the balance right?

The United Arab Emirates, with its investor-friendly policies, is the world’s third fastest emerging economy according to the Foreign Direct Investment Confidence Index and has emerged as an economic leader in the Middle East region. The UAE has grown by 7.6% in 2022, which showcases its economy’s strong comeback after the economic slumber caused by COVID-19.

New research from the Boston Consulting Group shows that the Emirates is expected to see financial wealth reach $800bn in 2027 with an annual growth rate of almost ten per cent.

The country has excellent infrastructure, including world-class ports and airports, making it easy for investors to transport goods and services across the globe. In addition, the UAE has invested heavily in its transportation and logistics infrastructure, making it an important hub for global trade.

In 2020, UAE changed its company law by allowing 100% foreign investments in most business activities (except Activities of Strategic Effect). This removed a major block for the foreign investors legally bound to involve UAE nationals in their investments in the country. This measure will bring new players to the market previously dominated by UAE nationals

The UAE has recently been actively pursuing bilateral trade agreements with countries worldwide. These agreements aim to boost trade and investment flows between the UAE and its trading partners while providing a platform for deeper economic cooperation. For example, the recent agreements signed with India, the UK, Israel, South Africa and Turkey along with the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) are expected to positively impact the UAE’s economy by increasing trade and investment flows in a range of sectors.

For instance, a year after signing India-UAE Comprehensive Economic Partnership Agreement, bilateral trade between the two nations grew by 27.5%. The UAE’s foreign trade hit 2.2 trillion dirhams ($599 billion) in 2022, up 17% on the year, while it has signed bilateral trade agreements with global partners spanning India, Israel and Indonesia.

In 2021, the United Arab Emirates, to celebrate the 50th anniversary of the nation, launched a series of programmes to stimulate and diversify its economy, seeking to attract some $150 billion in new foreign investment in the coming decade. These fifty new projects and initiatives included easing visa regulations to attract foreign workers, measures to boost technological development in the country, attracting software engineers and coders, along with other steps to increase trade.

The rapidly-changing regulatory environment is one of the biggest challenges businesses face in the UAE.

The government constantly introduces new laws and regulations, and businesses must comply with these. This can be time-consuming and expensive, particularly for small and medium-sized enterprises (SMEs) with limited resources. Additionally, the legal system in the UAE can be complex and opaque, making it difficult for businesses to navigate.

These regulations have been implemented to ensure businesses operate transparently and responsibly while protecting the interests of investors, customers and employees.

The increased flow of money brings a risk of increased illegal activities including money-laundering and terror financing. To mitigate these risks, the UAE has enacted several laws and regulations known as the Anti-Money Laundering (AML) and Combating Financing of Terrorism (CFT) laws. These measures include conducting customer due diligence, maintaining accurate records and reporting suspicious transactions to the relevant authorities.

UAE has created a mechanism to recognise an entity’s Ultimate Beneficiary Owners (UBOs), which requires the business entities to maintain adequate and up-to-date information about their shareholders and their ultimate beneficiary owners. In addition, the UAE has also established the Financial Intelligence Unit, which is responsible for collecting and analysing information on money-laundering and terrorist financing activities in the country.

The UAE government 2021 also introduced massive changes to the labour laws, which aimed at curbing discrimination, forced labour, harassment and bullying. The law fixes working hours and provides detailed provisions related to maternity benefits for women. The UAE has also established a Labour Market Regulatory Authority, which monitors and enforces labour laws in the country.

The nation is fast becoming a hub of start-ups and technology-driven businesses, making the UAE a global leader in innovation in the coming years. As a result, it is moving away from the traditional energy-driven economic model and is becoming a top attractive investment site. However, businesses need regular guidance from experts to tackle the complex legal and compliance framework of each Emirate. To succeed in the UAE, businesses must understand these challenges and develop strategies to comply with the regulations while still achieving their business objectives. This may include investing in local expertise and careful planning and executing compliance strategies.

"class="material with-radius">ADGM Foundations Regime offers a compelling alternative to trusts for individuals, families, and corporations seeking financial planning and structuring solutions. This innovative framework allows High Net Worth Individuals, families, and businesses in the United Arab Emirates (UAE) to access a highly sought-after product from a world-class international financial centre for the first time.

ADGM Foundations serve a wide range of purposes, including wealth management and preservation, family succession planning, tax planning, asset protection, corporate structuring, and fulfilling public interest objectives. They provide a powerful mechanism for consolidating various family assets into a single top holding entity. By utilizing a Foundation to hold family assets—be it business interests, properties, financial investments, or other valuable holdings—clear instructions can be legally established for the transfer of these assets upon succession.

Benefits of a Foundation:

Enhanced Governance: ADGM Foundations adhere to international best practices and regulatory standards. The Foundation Council operates under statutory duties similar to those imposed on company directors, ensuring responsible and transparent decision-making. A Guardian supervises the Foundation Council to ensure compliance with the Foundation’s Charter and By-Laws. While the appointment of a Guardian is optional during the Founder’s lifetime, it becomes compulsory upon the Founder’s death, enhancing oversight and continuity.

Legal Personality: An ADGM Foundation possesses its own legal personality. This legal status empowers Foundations to engage in contracts and arrangements directly, providing greater flexibility and autonomy in managing assets and conducting business activities.

Separate Liability: The Foundation’s distinct legal personality ensures a separation of liability between the Founder and the Foundation itself. This separation shields the Founder’s personal assets from any potential claims or liabilities associated with the Foundation, offering an additional layer of protection.

Perpetual Existence: An ADGM Foundation enjoys perpetual existence beyond the Founder’s lifetime. This enduring nature provides certainty and continuity for ongoing arrangements, ensuring the Foundation’s objectives and legacy can be maintained for future generations.

Asset Protection and Succession Planning: ADGM Foundations Regulations incorporate firewall provisions specifically designed to protect beneficiaries’ rights and safeguard the Foundation’s assets. These provisions help shield the Foundation’s assets from bankruptcy claims, claims arising from divorce, and the impact of forced heirship rules, enhancing asset protection and preservation.

Establishing a Foundation provides a higher degree of certainty and confidence that assets will be distributed according to the Founder’s wishes, with the Foundation continuing perpetually after the Founder’s demise. ADGM Foundations are designed to be fast and straightforward to set up and manage, with clear ongoing reporting requirements and competitive pricing.

Key steps to establish an ADGM Foundation-

Define Objectives and Structure: Clearly outline the objectives, purpose, and governance structure of the Foundation. This includes drafting the Foundation Charter and By-Laws, which establish the rules and guidelines governing the Foundation’s operations.

Submit Application: Preparation and submission of the necessary documentation, including the Foundation’s Charter, By-Laws, and other relevant documents, to the ADGM regulatory authority. Compliance with applicable regulations and guidelines is crucial during this stage.

Compliance and Approval: ADGM regulatory authorities will review the application to ensure compliance with the Foundation regulations. Upon successful review and approval, the Foundation is incorporated, and a Certificate of Incorporation is issued.

Foundation Establishment and Operation: Once incorporated, the Foundation can commence its operations, manage assets, and engage in activities in accordance with its Charter and By-Laws.

We strongly recommend seeking guidance from legal advisors with expertise in setting up Foundations in ADGM as legal advisors can provide insights, assist with legal compliance, and help navigate the incorporation process.

Conclusion: The ADGM Foundations Regime offers individuals, families, and businesses the opportunity to leverage a secure and well-regulated platform for their financial planning and structuring needs. The regime empowers stakeholders with greater control over their assets, preserving wealth, and providing a robust framework for intergenerational succession planning. With its ease of use, flexibility, and adherence to international standards, the ADGM Foundations Regime stands as a valuable addition to the UAE’s financial ecosystem.

For more details or any guidance please feel free to contact us.

The Golden Visa programme enables eligible individuals and their families to reside in the UAE for extended periods, making it easier to run a business from the UAE. Previously, residency permits were usually linked to employment, making it difficult for business owners to retain talent and provide stability. The Golden Visa is a simple programme with very few restrictions.

Free Zones have been the backbone of business growth in the UAE with considerable advantages for businesses, such as 100% foreign ownership, tax exemptions, and streamlined processes. Each free zone specializes in a particular industry, such as technology, finance, media and logistics, enabling businesses to benefit from a supportive ecosystem tailored to their sector. These zones offer state-of-the-art infrastructure, access to global markets, and proximity to major transportation hubs, facilitating seamless operations and international trade.

The UAE has streamlined business setup procedures, reduced bureaucracy, and enhanced investor confidence. The establishment of online portals, such as the Abu Dhabi Business Center and Dubai Economy, allows entrepreneurs to complete procedures and obtain licences efficiently. The introduction of e-platforms and digital services has simplified administrative tasks, making it easier for businesses to operate.

The UAE has actively encouraged innovation and entrepreneurship. Initiatives such as the Dubai Future Accelerators and Dubai Startup Hub support startups, attract talent and facilitate collaboration between entrepreneurs, investors, and government entities. The government’s commitment to innovation is reflected in the creation of dedicated innovation districts, such as the Dubai Internet City and the Abu Dhabi Global Market. These provide ecosystems conducive to technological advances and business development.

Last year, the UAE and India signed a Comprehensive Economic Partnership Agreement, increasing the opportunities for India businesses to expand into the UAE market. Trade between the nations has increased by 27.5%, with a target of USD115 billion worth of trade within five years.

Tariffs have been reduced on a wide range of goods. The services sector has been liberalised in areas such as IT, finance, healthcare, tourism and education. Increased protection for investments in both directions has created a stable and secure environment for cross-border investments. Protection of intellectual property rights has been strengthened and general economic cooperation has led to joint ventures and collaboration.

Businesses can be set up through mainland companies, free zones, and offshore entities, each with particular advantages. Licences and approvals are available from government authorities for a wide range of activities, including trading, manufacturing and providing professional and other services. Comprehending the legal structure, understanding the market, adhering to regulations and embracing the local culture will lead to the establishment of a successful and thriving business.

The geographical proximity of India and the UAE, with deep cultural and historical connections, makes good business sense for companies from both to work together. Straightforward and credible UAE legal structures enable India companies to make global advances; UAE companies can enter the India market to reap the benefits of a thriving economy with robust manufacturing and fintech ecosystems.

Gautam Khurana Managing Partner India Law Offices"class="material with-radius">The United Arab Emirates (UAE) has been a favoured business destination for Indians for decades. Recent changes have made an even more compelling case for Indian companies to be in the UAE for their global capability centres (GCC) as well as for their international business needs. India enterprises should be aware of these developments to benefit from the UAE business ecosystem.

Foreign investors previously faced restrictions on ownership in various sectors. However, the UAE government has significantly reformed foreign direct investment rules and improved its international competitiveness. A key reform was theUAE Federal Decree by Law No. (26) of 2020, allowing foreign investors to own 100% of their businesses in certain sectors outside the free zones. Foreign companies can now establish a presence in the UAE without having a local partner, boosting economic growth and diversification.

The Golden Visa programme enables eligible individuals and their families to reside in the UAE for extended periods, making it easier to run a business from the UAE. Previously, residency permits were usually linked to employment, making it difficult for business owners to retain talent and provide stability. The Golden Visa is a simple programme with very few restrictions.

Free Zones have been the backbone of business growth in the UAE with considerable advantages for businesses, such as 100% foreign ownership, tax exemptions, and streamlined processes. Each free zone specializes in a particular industry, such as technology, finance, media and logistics, enabling businesses to benefit from a supportive ecosystem tailored to their sector. These zones offer state-of-the-art infrastructure, access to global markets, and proximity to major transportation hubs, facilitating seamless operations and international trade.

The UAE has streamlined business setup procedures, reduced bureaucracy, and enhanced investor confidence. The establishment of online portals, such as the Abu Dhabi Business Center and Dubai Economy, allows entrepreneurs to complete procedures and obtain licences efficiently. The introduction of e-platforms and digital services has simplified administrative tasks, making it easier for businesses to operate.

The UAE has actively encouraged innovation and entrepreneurship. Initiatives such as the Dubai Future Accelerators and Dubai Startup Hub support startups, attract talent and facilitate collaboration between entrepreneurs, investors, and government entities. The government’s commitment to innovation is reflected in the creation of dedicated innovation districts, such as the Dubai Internet City and the Abu Dhabi Global Market. These provide ecosystems conducive to technological advances and business development.

Last year, the UAE and India signed a Comprehensive Economic Partnership Agreement, increasing the opportunities for India businesses to expand into the UAE market. Trade between the nations has increased by 27.5%, with a target of USD115 billion worth of trade within five years.

Tariffs have been reduced on a wide range of goods. The services sector has been liberalised in areas such as IT, finance, healthcare, tourism and education. Increased protection for investments in both directions has created a stable and secure environment for cross-border investments. Protection of intellectual property rights has been strengthened and general economic cooperation has led to joint ventures and collaboration.

Businesses can be set up through mainland companies, free zones, and offshore entities, each with particular advantages. Licences and approvals are available from government authorities for a wide range of activities, including trading, manufacturing and providing professional and other services. Comprehending the legal structure, understanding the market, adhering to regulations and embracing the local culture will lead to the establishment of a successful and thriving business.

The geographical proximity of India and the UAE, with deep cultural and historical connections, makes good business sense for companies from both to work together. Straightforward and credible UAE legal structures enable India companies to make global advances; UAE companies can enter the India market to reap the benefits of a thriving economy with robust manufacturing and fintech ecosystems.

To read the full IR Global Publication, kindly click here

"class="material with-radius">The United Arab Emirates, with its investor-friendly policies, is the third most global emerging economy in the world as per Foreign Direct Investment Confidence Index and has emerged as an economic leader in the middle east region.

The UAE has grown by 7.6% in 2022, which showcases its economy’s strong comeback after the economic slumber caused by Covid-19. The country has excellent infrastructure, including world-class ports and airports, making it easy for investors to transport goods and services across the globe. In addition, the UAE has invested heavily in its transportation and logistics infrastructure, making it an important hub for global trade.

In 2020, UAE changed its company law by allowing 100% foreign investments in most business activities (except Activities of Strategic Effect). This removed a major block for the foreign investors legally bound to involve UAE nationals in their investments in the country. This measure will bring new players to the market previously dominated by UAE nationals.

The UAE has been actively pursuing bilateral trade agreements with countries worldwide recently. These agreements aim to boost trade and investment flows between the UAE and its trading partners while providing a platform for deeper economic cooperation. For example, the recent agreements signed with India, the UK, Israel, South Africa, and Turkey and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) are expected to positively impact the UAE’s economy by increasing trade and investment flows in a range of sectors. For instance, a year after signing India-UAE Comprehensive Economic Partnership Agreement, bilateral trade between the two nations grew by 27.5%. The UAE’s foreign trade hit 2.2 trillion dirhams ($599 billion) in 2022, up 17% yearly, and it has signed bilateral trade agreements with global partners spanning India, Israel and Indonesia.

In 2021, the United Arab Emirates, to celebrate the 50th anniversary of the nation, launched a series of programs to stimulate and diversify its economy, seeking to attract some $150 billion in new foreign investment in the coming decade. These fifty new projects and initiatives included easing visa regulations for attracting foreign workers, measures to boost technological development in the country, attracting software engineers and coders, and other measures to increase trade.

The rapidly changing regulatory environment is one of the biggest challenges businesses face in the UAE. The government constantly introduces new laws and regulations, and businesses must comply with these laws. This can be time-consuming and expensive, particularly for small and medium-sized enterprises (SMEs) with limited resources.

Additionally, the legal system in the UAE can be complex and opaque, making it difficult for businesses to navigate. These regulations have been implemented to ensure businesses operate transparently and responsibly while protecting stakeholders’ interests, such as investors, customers, and employees. The increased flow of money brings a risk of increased illegal activities like money laundering and terror financing. To mitigate these risks, the UAE has enacted several laws and regulations to combat them known as the Anti-Money Laundering (AML) and Combating Financing of Terrorism (CFT) laws. These measures include conducting customer due diligence, maintaining accurate records, and reporting suspicious transactions to the relevant authorities. UAE has created a mechanism to recognise an entity’s Ultimate Beneficiary Owners (UBOs), which requires the business entities to maintain adequate and up-to-date information about their shareholders and the ultimate beneficiary owners.

In addition, the UAE has also established the Financial Intelligence Unit, which is responsible for collecting and analysing information on money laundering and terrorist financing activities in the country. The UAE government 2021 also introduced massive changes to the labour laws, which aimed at curbing discrimination, forced labour, harassment, and bullying. The law fixes working hours and provides detailed provisions related to maternity benefits which women can avail of. The UAE has also established a Labor Market Regulatory Authority, which monitors and enforces labour laws in the country. The nation is fast becoming a hub of startups and technology-driven businesses, making UAE a global leader in innovation in the coming years. As a result, it is moving away from the traditional energy-driven economic model and is becoming a top attractive investment site. However, businesses need regular guidance from experts to tackle the complex legal and compliance framework of each Emirate. To succeed in the UAE, businesses must understand these challenges and develop strategies to comply with the regulations while still achieving their business objectives. This may include investing in local expertise and careful planning and executing compliance strategies.

"class="material with-radius">SUMMARY: 1. The case 2. Introduction – 3. The scope of the 1999 Geneva Convention

1. – A Chinese customer requests urgent protection, he has chartered a vessel (transporting

petrochemicals) flying the Hong Kong flag.

Once the transport was completed, neither the remainder of the expenditure for the galley (bunker), nor

the spare parts (total of the credit requested in return, 350,000.00 euros) was returned to the customer.

We have discovered through the AIS system that the ship was sailing in Italian waters, near Genoa, which thus becomes the Court competent for the seizure, seizure which is notifed

by the Coast Guard, Port Authority. The activity is aimed at inducing the debtor to quickly pay the total amount or most of it in order not to have the ship seized for a long period.

2. – The seizure of a ship is mainly an instrument of the creditor who often remains without enforceable

title and is forced to use this measure to ensure the realization of his credit by preventing the debtor from carrying out dispositions capable of reducing the consistency of his own heritage. In maritime credits, reference is often made to preventing the departure of the debtor’s ship which remains stranded at the port

3. – The first international text which led to the unification of the rules on the institution of the precautionary attachment of seagoing vessels was the Brussels Convention of 1952 drawn up on the

initiative of the Comité Maritime International. The Brussels Convention, following the Anglo-Saxon model, allows the ship to be attached only for certain maritime credits and on the condition that they are strictly connected with the seized ship and also burden the ship owner both at the time the credit is born and at the time when the seizure is carried out. Exceptionally and with limitations, the seizure of the “sister ship” is also permitted, as well as the ship that has been transferred to a third party during the seizure.

The new Convention adopted on March 12, 1999 on the attachment of ships, entered into force on September 14, 2011. However, to date the majority of States with significant shipping traffic have remained in the application of the provisions of the 1952 Convention.

The new Convention contains provisions which sanction the scope of application in a far more extensive

way than what was established by the provision of art. 2 of the 1952 Convention. Precisely, according to

the provisions of articles 2 §1 and 8 §1 of the new Convention, the court of a Contracting State may order the seizure of a ship or the revocation of the same regardless of whether the ship belonged to a Contracting State or not.

The conservative seizure is ordered even if in the clause having jurisdiction or in the arbitration clause it

had been agreed otherwise, i.e. that the claim would be brought before the Court of a State other than the

one where the seizure was carried out and would be decided according to the rules of that State (art. 2

§3). The 1999 Geneva Convention contains an extensive list of definitions and terms used, with all the

necessary additions to the 1952 Convention. In addition to the term ‘detention’, the new Convention also

refers to the ‘restriction on removal’ to offer solutions to legislations that do not provide for the detention

of ships in their rules and to also include the development that took place in Anglo-Saxon law with the “

Mareva Injunction” “Freezing Orders” of the Civil Procedure Rules 1999 19.

">[1] The DFSA Conduct of Business Module Rulebook has set out certain obligations for platform operators related to investors and borrowers/issuers.

For Investors

Risks Involved

The regulations aim at educating the prospective investor or the lender about the inherent risks associated with Crowdfunding since the seekers of such investments are mostly new business ideas. Hence there is an inherent risk of loss involved while investing in these businesses.

The crowdfunding platform has an obligation to make investors aware of such risks through disclaimers. For instance, the DFSA rulebook obligates the platforms to disclose detailed information about past loan defaults that have occurred on the platform.[2]

Other information

The crowdfunding operator must make the investors aware of the functionality of the platform and make them aware of the following:[3]

How the platform is remunerated,

Eligibility criteria for investors and lenders as well as issuers and borrowers,

Minimum and maximum value of investment or loan that could be provided,

Procedure for withdrawal of investment,

Measures for data protection

The platforms cannot use a single legal entity to provide regulated and unregulated crowdfunding services. Since these regulations apply to investments and loans, the platform must not be utilised to seek donations.[4]

For Issuers and Borrowers

The platform must conduct due diligence to ensure correct information about the identity of such individuals or body corporates. The platform must seek their business proposals and ensure the commitment and expertise of the individuals involved in the business they seek funds for.[5]

"class="material with-radius">[1] The DFSA Conduct of Business Module Rulebook has set out certain obligations for platform operators related to investors and borrowers/issuers.

For Investors

Risks Involved

The regulations aim at educating the prospective investor or the lender about the inherent risks associated with Crowdfunding since the seekers of such investments are mostly new business ideas. Hence there is an inherent risk of loss involved while investing in these businesses.

The crowdfunding platform has an obligation to make investors aware of such risks through disclaimers. For instance, the DFSA rulebook obligates the platforms to disclose detailed information about past loan defaults that have occurred on the platform.[2]

Other information

The crowdfunding operator must make the investors aware of the functionality of the platform and make them aware of the following:[3]

How the platform is remunerated,

Eligibility criteria for investors and lenders as well as issuers and borrowers,

Minimum and maximum value of investment or loan that could be provided,

Procedure for withdrawal of investment,

Measures for data protection

The platforms cannot use a single legal entity to provide regulated and unregulated crowdfunding services. Since these regulations apply to investments and loans, the platform must not be utilised to seek donations.[4]

For Issuers and Borrowers

The platform must conduct due diligence to ensure correct information about the identity of such individuals or body corporates. The platform must seek their business proposals and ensure the commitment and expertise of the individuals involved in the business they seek funds for.[5]

e-Commerce sales have been taking constant giant leaps starting from 2020. Moreover, the year 2020 brought lockdown and social distancing protocols that led to an instant surge in the registration of online business licenses. In just the first few months of that year, the consumer demand for online business services increased a great deal. By 2025, the UAE market’s population is expected to have access to the internet and mobile devices at a rate of about 100 percent, according to the Dubai Chamber of Commerce and Industry.

With consumers prioritizing their satisfaction in the products and services they purchase, the e-commerce industry continues to grow faster. Since the pandemic, the use of online payment apps has also increased at many outlets, markets, taxis, theatres, etc. As per the recent data, 30% of the UAE’s population are known as digital natives who have raised the volume of online shopping. The UAE government’s Smart Dubai 2021 initiative to build a robust digital economy is also praiseworthy. UAE is certainly growing at a rapid pace to explore the exclusive potential of the e-Commerce market.

e-Commerce sales have been taking constant giant leaps starting from 2020. Moreover, the year 2020 brought lockdown and social distancing protocols that led to an instant surge in the registration of online business licenses. In just the first few months of that year, the consumer demand for online business services increased a great deal. By 2025, the UAE market’s population is expected to have access to the internet and mobile devices at a rate of about 100 percent, according to the Dubai Chamber of Commerce and Industry.

With consumers prioritizing their satisfaction in the products and services they purchase, the e-commerce industry continues to grow faster. Since the pandemic, the use of online payment apps has also increased at many outlets, markets, taxis, theatres, etc. As per the recent data, 30% of the UAE’s population are known as digital natives who have raised the volume of online shopping. The UAE government’s Smart Dubai 2021 initiative to build a robust digital economy is also praiseworthy. UAE is certainly growing at a rapid pace to explore the exclusive potential of the e-Commerce market.

"class="material with-radius">The United Arab Emirates (UAE) with its exotic shopping malls is a prime attraction point for shoppers. If tourists buy products from a shop participating in the ‘Tax Refund for Tourists Scheme’ they can claim refunds for the Value Added Tax paid on the products. This scheme is only available for individuals leaving the country within 90 days of buying such products. The tourists can claim the refund at the airports by submitting the invoices along with copies of their credit card and passport. A refund can be claimed either in cash or on the credit card itself.

To attract tourists, the UAE government has come up with a ‘five-year multiple-entry tourist visa’. A five-year-long visa would enable individuals to keep visiting the UAE without the hassle of going through the visa process. However, tourists cannot work on this visa and shall have to apply for a work or employment visa if they wish to work. Any violation could result in deportation and fines. However, individuals can look for jobs while on a visit visa and can apply for a work visa through their employers in case they secure a job.

The impressive public transport in the UAE is used extensively by locals and tourists. However, not many are aware that an individual caught eating or drinking while using public transport could be fined up to AED 100.

Swearing in public causing harm to the honor or dignity of an individual could also result in a fine up to AED 20,000 or imprisonment up to one year. The punishment for addressing such insults to a public servant could result in a fine of up to AED 50,000 along with the punishment of up to two years.

Taking pictures of an individual without his or her permission is considered a serious issue of invasion of privacy and the law provides for a punishment of up to 1 year and a fine of up to AED 500,000. Sharing pictures of a road accident on social media is also considered a serious crime. Both these acts could also result in the deportation of the individual.

"class="material with-radius">In the year 2015, the United Arab Emirates (UAE) government established a federal entity by the name of Gender Balance Council to develop and implement the gender balance agenda in the country. The council aimed at increasing female participation in decision-making positions. The overall objective was to position the UAE as a model for gender equality across the globe. In 2018, the president of the UAE passed a decree to ensure 50% women representation in the Federal National Council, a constitutional body responsible for passing, amending, or rejecting federal draft laws and having several other important powers.

In 2019, the UAE also introduced legal provisions to curb domestic violence acts, imposing a punishment of up to six months or a fine of AED 5000 or both. The abuse includes not just acts of physical violence but also sexual, economic, and emotional abuse of the spouse. The law also provides for obtaining restraining orders to disable the abusive individual from making untoward efforts to meet the complainant or the children. Breaching the restraining order carries a three-month jail sentence or/and fine between AED 1000 to 10,000.

In 2020, the UAE government introduced changes to its Federal Law No 8 of 1980. Newly introduced Article 32 provided for an equal wage for equal work to a female worker. The amendment is an important step for reducing the wage gap between men and women performing the same work or work of equal value.